Here’s an uncomfortable truth about sustainability reports: without third-party verification, they’re basically trust-me documents.

A company can publish a beautifully designed 80-page report full of emissions data, diversity metrics, and water-usage statistics — and every single number could be wrong, misleading, or cherry-picked.

Without a qualified third party checking the work, there’s no way for investors, regulators, or customers to know the difference.

That’s where third-party verification comes in. It’s the process of having an independent expert review your sustainability data and disclosures to confirm they’re accurate, complete, and aligned with recognized standards.

Think of it as the sustainability equivalent of a financial audit.

And in 2026, it’s no longer optional for a growing number of organizations.

New regulations in Europe, California, and across dozens of other jurisdictions are making third-party verification of sustainability reports a legal requirement — not a nice-to-have.

This guide breaks down everything you need to know: what third-party verification actually involves, why it’s becoming mandatory, which standards govern the process, and how to prepare your organization without losing your mind (or your budget) along the way.

What Is Third-Party Verification of a Sustainability Report?

Third-party verification — also called external assurance — is a formal, structured review of your sustainability disclosures conducted by an independent organization.

The verifier examines your data, your data-collection processes, and the claims you make in your report to determine whether they’re materially accurate and consistent with the reporting standards you’ve chosen to follow.

The key word here is independent. The whole point is that the reviewer has no financial stake in the outcome.

They’re not your consultant, your board member, or your marketing team.

They’re an outside expert whose job is to tell the truth about the quality of your disclosures — even when the truth isn’t flattering.

The output of the process is an assurance statement (sometimes called a verification statement or assurance opinion) that gets published alongside your sustainability report.

This statement tells your stakeholders whether a qualified professional reviewed your data and what level of confidence they can place in it.

Verification vs. Validation vs. Certification: What’s the Difference?

These terms get mixed up constantly, so let’s clear them up:

- Verification confirms that the information in your report is accurate and complete — it looks backward at what you’ve already reported.

- Validation assesses whether forward-looking claims (like emissions reduction targets or net-zero commitments) are credible and based on sound methodology.

- Certification means your organization or product has met the requirements of a specific standard (like ISO 14001 or B Corp) and has been formally approved by an accredited body.

Third-party verification of a sustainability report is specifically about checking the accuracy of what you’ve already disclosed. It’s a backward-looking accuracy check, not a forward-looking endorsement.

Why Third-Party Verification Matters More Than Ever

The Greenwashing Problem

Let’s be direct: the sustainability space has a credibility problem.

Too many companies have made vague or exaggerated environmental claims without the data to back them up.

The EU Green Claims Directive is specifically designed to crack down on unsubstantiated sustainability marketing, and regulators in the UK, Canada, and the United States are following suit.

Third-party verification is the antidote.

When an independent expert confirms that your numbers are sound, it separates your organization from the noise.

It tells investors, customers, and regulators that you’re not just saying the right things — you’re proving them.

Regulatory Pressure Is Real

The regulatory landscape has shifted dramatically. Here’s where things stand in 2026:

- EU CSRD: Companies reporting under the Corporate Sustainability Reporting Directive must obtain limited assurance on their full sustainability statement. The first wave of reports — covering the largest companies — was published in 2025, with subsequent waves phasing in through 2028. The EU plans to move toward mandatory reasonable assurance in the coming years.

- California SB 253: Companies with over $1 billion in annual revenue doing business in California must report Scope 1 and 2 emissions with limited assurance starting in 2026, escalating to reasonable assurance by 2030.

- ISSB adoption: Over 35 jurisdictions have adopted or are implementing the ISSB Standards, and several are incorporating assurance requirements into their local regulations.

- ISSA 5000: The International Auditing and Assurance Standards Board published a new global standard specifically for sustainability assurance — ISSA 5000 — effective for reporting periods beginning on or after December 15, 2026. This replaces the older ISAE 3000 for sustainability engagements and sets a unified global benchmark.

Investor and Stakeholder Expectations

Even outside of mandatory requirements, the market is moving.

Over 85% of chief investment officers now consider ESG factors as indicators of long-term value, and verified data is increasingly a baseline expectation. CDP, the world’s largest environmental disclosure platform, aligns its scoring methodology with assurance expectations.

ESG rating agencies give higher marks to companies with externally assured reports.

Put simply: if you’re publishing sustainability data that hasn’t been independently checked, a growing number of stakeholders will discount it — or ignore it entirely.

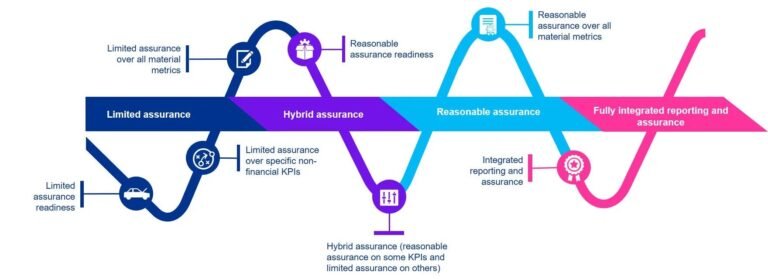

Limited vs. Reasonable Assurance: Understanding the Two Levels

Not all verification is created equal. There are two distinct levels of assurance, and understanding the difference is critical for choosing the right approach for your organization.

What Is Limited Assurance?

Limited assurance is the lighter-touch option.

The verifier reviews your data, tests a sample of your processes, and determines whether anything came to their attention that suggests the information is materially misstated.

The conclusion is expressed in negative form: “Nothing has come to our attention that causes us to believe the sustainability information is materially misstated.”

Think of it as a focused plausibility check. The verifier isn’t saying your data is definitely correct — they’re saying they didn’t find evidence that it’s wrong.

Limited assurance typically involves testing 10–20% of your data points and reviewing your collection methodology at a high level.

What Is Reasonable Assurance?

Reasonable assurance is the gold standard — the sustainability equivalent of a full financial audit.

The verifier conducts significantly more testing, examines source documentation in depth, evaluates your underlying assumptions and calculation methodologies, and provides a positive conclusion: “In our opinion, the sustainability information is presented fairly, in all material respects, in accordance with the applicable reporting criteria.”

This is a much more rigorous (and more expensive) process.

It requires comprehensive evidence gathering, cross-verification against primary sources like utility bills, fuel receipts, and meter readings, and a thorough evaluation of your internal controls.

Which Level Should You Choose?

For most organizations getting started with verification, limited assurance is the practical starting point.

It’s what the CSRD currently requires, it’s less costly, and it’s achievable even if your data systems aren’t yet fully mature.

Reasonable assurance makes sense for organizations that want to demonstrate the highest level of credibility, face intense investor scrutiny, or are preparing for regulations that will eventually mandate it (California’s SB 253 timeline moves to reasonable assurance by 2030, for example).

Many companies follow a phased approach: start with limited assurance to build systems and processes, then graduate to reasonable assurance as their data infrastructure matures.

Common Verification Standards and Frameworks

Several recognized standards govern how third-party assurance engagements are conducted. Here are the ones you’re most likely to encounter.

ISSA 5000 (The New Global Benchmark)

Published by the International Auditing and Assurance Standards Board in late 2024, ISSA 5000 is the first international standard designed specifically for sustainability assurance.

It becomes effective for reporting periods beginning on or after December 15, 2026, and is expected to become the dominant global standard.

ISSA 5000 is framework-neutral, meaning it works with any sustainability reporting standard — GRI, ESRS, ISSB, or others.

It covers both limited and reasonable assurance, addresses forward-looking information and value-chain data, and accommodates both single and double materiality concepts.

Jurisdictions including Australia, Canada, the UK, Hong Kong, South Africa, and others have already adopted or are in the process of adopting local equivalents.

ISAE 3000 (Revised)

Until ISSA 5000 takes effect, ISAE 3000 remains the most widely used standard for sustainability assurance globally.

Issued by the IAASB, it’s a general-purpose assurance standard that was designed for non-financial information broadly — not exclusively for sustainability.

Once ISSA 5000 becomes effective, ISAE 3000 will no longer apply to sustainability engagements, though it will continue to govern assurance on other non-financial subject matters.

AA1000 Assurance Standard (v3)

Published by AccountAbility, the AA1000AS is unique because it evaluates not just data accuracy, but also an organization’s adherence to stakeholder engagement principles: inclusivity, materiality, responsiveness, and impact.

It’s particularly popular with organizations that prioritize stakeholder-centric reporting and want their assurance process to assess the quality of their engagement practices, not just their numbers.

ISO 14064-3

If your third-party verification needs are specifically focused on greenhouse gas emissions, ISO 14064-3 provides guidance for the validation and verification of GHG assertions.

It’s commonly used alongside broader assurance standards when emissions data is a key component of the report.

What the Verification Process Actually Looks Like

If you’ve never been through a sustainability assurance engagement, here’s what to expect. The process typically unfolds in five stages.

Stage 1: Scoping and Planning

Before any data gets reviewed, you and your assurance provider agree on the scope of the engagement.

This includes which parts of your report will be verified, which reporting standards are being applied, whether the engagement will be limited or reasonable assurance, and the timeline and logistics.

This is also when the verifier assesses the reporting boundaries — which entities, operations, and geographies are included — and identifies the areas of highest risk for material misstatement.

Stage 2: Document Review and Risk Assessment

The verifier reviews your sustainability report alongside the supporting documentation: data collection spreadsheets, calculation methodologies, source records (utility bills, invoices, HR databases, supplier questionnaires), and any internal audit results.

They identify where the data comes from, how it flows through your systems, and where the risks of error or omission are highest.

Stage 3: Testing and Evidence Gathering

This is the core of the engagement. The verifier tests a sample of your data points by tracing them back to primary sources. For a limited assurance engagement, this might involve testing 10–20% of your key metrics.

For reasonable assurance, the testing is significantly more comprehensive.

The verifier also evaluates your internal controls — the processes and checks you have in place to ensure data quality.

They’re looking at whether you have clear data ownership, documented calculation methodologies, appropriate quality-assurance checks, and a reliable audit trail.

Stage 4: Findings and Management Response

If the verifier identifies errors, inconsistencies, or gaps, they’ll raise them with your team.

Depending on the severity, you may have the opportunity to correct issues before the final report is published.

Minor findings might result in recommendations for improvement. Material findings could affect the assurance opinion itself.

Stage 5: Assurance Statement

The final output is a formal assurance statement that accompanies your published sustainability report.

It describes the scope of the engagement, the standard used, the level of assurance provided, the verifier’s conclusion, and any qualifications or observations.

This is the document your investors, regulators, and other stakeholders will reference when evaluating the credibility of your disclosures.

Key Benefits of Third-Party Verification

Beyond regulatory compliance, third-party verification delivers tangible strategic value.

- Stakeholder trust: Verified data tells investors, customers, and regulators that your sustainability claims have been independently checked. Research has shown that companies with externally assured sustainability reports enjoy a measurable reduction in their cost of capital.

- Greenwashing protection: In an era of tightening anti-greenwashing regulations, an assurance statement provides a layer of legal and reputational protection. It demonstrates that your claims are grounded in evidence, not aspiration.

- Improved internal data quality: The assurance process almost always reveals gaps, inconsistencies, and opportunities to improve how you collect and manage sustainability data. Many companies find that the biggest value of verification isn’t the statement itself — it’s the internal improvements that come from preparing for it.

- Competitive differentiation: In crowded markets, externally verified sustainability performance is a genuine differentiator. It signals operational maturity and long-term thinking — qualities that matter to institutional investors and enterprise buyers alike.

- Future-proofing: Starting with voluntary assurance now builds the systems, processes, and internal capabilities you’ll need when mandatory requirements arrive. Organizations that wait until the last minute typically face compressed timelines, higher costs, and painful data gaps.

How to Choose the Right Assurance Provider

Not all verification providers are equal, and choosing the right partner matters. Here are the criteria that should guide your decision.

Accreditation and Qualifications

Look for providers accredited under recognized schemes — ISO 17021 for management systems, ISO 14065 for greenhouse gas verification, or licensed under the relevant professional accounting standards for financial assurance.

The Big Four accounting firms (Deloitte, PwC, EY, KPMG) all offer sustainability assurance services, as do specialized verification bodies like Bureau Veritas, SGS, and DNV.

Industry Experience

Sustainability risks and metrics vary significantly by sector.

A verifier with deep experience in your industry will understand the specific data challenges, materiality thresholds, and regulatory nuances you face.

Ask for references from organizations of similar size and sector.

Approach and Methodology

Evaluate whether the provider takes a collaborative approach or a purely compliance-checking stance. The best assurance partners act as constructive critics — identifying issues while helping you build stronger data systems.

Many organizations also benefit from engaging a dedicated sustainability data management platform to centralize their ESG data, automate audit trails, and ensure that information is verification-ready before the assurance engagement begins.

Capacity and Timing

With demand for sustainability assurance surging, qualified providers are increasingly in short supply. Engage your preferred partner early — ideally 6–12 months before you plan to publish your report.

Waiting until the last minute risks scrambling for availability and paying premium rates.

Cost Considerations

Assurance costs vary widely depending on the scope of the engagement, the level of assurance, the complexity of your operations, and the provider’s fee structure.

As a rough benchmark, limited assurance engagements for mid-sized companies typically range from $30,000 to $80,000, while reasonable assurance can run from $75,000 to well over $200,000.

These are significant investments — but the cost of publishing unverified data in an increasingly regulated environment can be far higher.

How to Get Your Organization Audit-Ready

Preparation is everything. The smoother your internal systems and processes are before the verifier arrives, the faster, cheaper, and less painful the assurance engagement will be.

Build Source-Level Traceability

Every data point in your sustainability report needs a clear audit trail linking it back to primary documentation: utility bills, fuel receipts, equipment logs, supplier questionnaires, HR records, and so on.

If the verifier asks “where did this number come from?” you need a documented, traceable answer.

Document Your Methodologies

Don’t just report numbers — document how you calculated them.

Which emission factors did you use?

What organizational boundaries did you apply?

How did you handle data gaps or estimates?

What assumptions underlie your Scope 3 calculations?

A clear methodology document saves enormous time during the assurance process.

Invest in the Right Technology

Modern ESG reporting is too data-intensive for spreadsheets alone.

A purpose-built ESG audit and compliance platform can automate data collection, enforce consistent methodologies, flag anomalies, and generate the structured, audit-ready outputs that verification providers need.

This isn’t a luxury — it’s a prerequisite for efficient assurance at scale.

Run an Internal Pre-Assessment

Before engaging an external verifier, conduct your own internal review. Identify gaps, inconsistencies, and areas where documentation is weak.

Many organizations find that a structured internal dry run reveals 80% of the issues that an external verifier would flag — giving you the chance to fix them before the formal engagement begins.

If your internal team lacks the capacity or expertise for a thorough pre-assessment, bringing in a specialist ESG assurance readiness consultant to conduct a gap analysis can prevent costly surprises during the formal verification process.

Train Your Team

Your sustainability team needs to understand not just what to report, but how to prepare data for external scrutiny.

Investing in a focused sustainability assurance training course can build the practical skills your staff needs — from audit-trail documentation to engaging effectively with verifiers — without pulling them out of their day-to-day responsibilities for weeks at a time.

Common Pitfalls to Avoid

Organizations going through their first assurance engagement often stumble on the same issues. Here’s what to watch for.

- Starting too late: Building verification-ready data systems takes time. If your reporting deadline is six months away and you haven’t started preparing, you’re already behind. Begin at least 12 months before your target publication date.

- Treating assurance as a compliance box-check: The organizations that get the most value from verification treat it as a strategic improvement process, not a regulatory obligation. Use the findings to genuinely strengthen your data quality and reporting practices.

- Underestimating Scope 3 complexity: Value-chain emissions data is inherently harder to verify because it relies on information from suppliers and other third parties. Start collecting and documenting Scope 3 data early, and work with your supply chain partners to improve data quality over time.

- Choosing a provider based solely on price: The cheapest assurance provider may not have the industry expertise, capacity, or methodological rigor your organization needs. A poorly conducted assurance engagement can actually damage credibility rather than enhance it.

- Ignoring qualitative disclosures: Verification doesn’t just cover numbers. Your governance descriptions, risk management narratives, and stakeholder engagement claims can also be examined. Make sure these qualitative sections are accurate and supported by documentation, not just polished prose.

Looking Ahead: The Future of Sustainability Assurance

The trajectory is clear. Sustainability assurance is converging toward the same level of rigor, standardization, and regulatory expectation that governs financial auditing.

ISSA 5000 is the first purpose-built global standard for sustainability assurance, and it signals a fundamental shift: sustainability data is now expected to be treated with the same discipline as financial data.

The EU is already planning the move from limited to reasonable assurance under the CSRD.

California’s timeline escalates to reasonable assurance by 2030. And jurisdictions across Asia, Africa, and Latin America are adopting local equivalents of ISSA 5000 at a rapid pace.

For organizations that haven’t yet begun their assurance journey, the message is straightforward: start now.

The tools are better than ever. Standards like ISSA 5000 provide clear, globally consistent guidance. And the market for qualified assurance providers, while tightening, is still accessible to companies that plan ahead.

Investing in a reliable sustainability reporting and assurance solution early in your reporting cycle can dramatically reduce the cost and complexity of the verification process later.

Final Thoughts: Verification Is Credibility

A sustainability report without third-party verification is like a financial statement without an audit — it might be accurate, but nobody can be sure.

And in a world where trust is the scarcest resource in corporate sustainability, that uncertainty is a liability you can’t afford.

Verification doesn’t have to be painful. It doesn’t have to be prohibitively expensive.

And it doesn’t have to wait until regulators force your hand. What it does require is preparation, the right technology, a qualified partner, and a genuine commitment to getting your data right — not just getting your report published.

The organizations that embrace verification early aren’t just checking a compliance box.

They’re building the data infrastructure, internal capabilities, and stakeholder trust that will define competitive advantage in the years ahead. That’s not a cost. That’s an investment.

Wondering whether your sustainability report is ready for third-party verification? At Sustaenia, we help organizations build verification-ready ESG reporting systems with clarity and confidence. Get in touch to start the conversation.