If you’ve spent any time researching sustainability reporting, you’ve probably run into a wall of acronyms: GRI, SASB, TCFD, ISSB, CSRD, CDP… the list goes on.

It’s enough to make even a seasoned business leader’s eyes glaze over.

Here’s the good news. You don’t need to master every single framework on the planet.

You just need to understand the three that have shaped the modern ESG reporting landscape more than any others — the Global Reporting Initiative (GRI), the Sustainability Accounting Standards Board (SASB), and the Task Force on Climate-related Financial Disclosures (TCFD) — and figure out which combination makes sense for your organization.

In this guide, we’ll break down each framework in plain language, explain who it’s designed for, compare them side by side, and help you choose the right path forward. No jargon. No alphabet-soup headaches. Just practical advice you can actually use.

Why ESG Reporting Frameworks Exist (And Why You Should Care)

Think of ESG reporting frameworks as the grammar rules of sustainability communication.

Without them, every company would describe its environmental and social performance in its own way, using its own metrics, making it nearly impossible for investors, customers, or regulators to compare one company to another.

That’s exactly what was happening a decade ago.

Companies published glossy sustainability reports with impressive-sounding numbers, but there was no consistency, no comparability, and very little accountability.

Frameworks solved that problem by creating standardized structures for what to report, how to measure it, and who the information is really for. And that last part — the intended audience — is actually the single most important factor when choosing a framework.

The global ESG regulatory landscape has tightened dramatically.

The EU’s Corporate Sustainability Reporting Directive (CSRD) now mandates detailed disclosures from tens of thousands of companies.

The ISSB has been adopted or is being implemented in more than 35 countries. And California’s climate disclosure laws are pushing emissions reporting forward in the United States even while federal rules remain uncertain.

For organizations of every size, understanding these frameworks isn’t optional anymore. It’s foundational to credibility, compliance, and competitive advantage.

GRI: The Global Standard for Stakeholder Transparency

What It Is

The Global Reporting Initiative, or GRI, is one of the oldest and most widely used sustainability reporting frameworks in the world.

Launched in the late 1990s, it has grown into a comprehensive set of modular standards that guide organizations in disclosing their environmental, social, and governance impacts.

As of 2025, more than 14,000 organizations worldwide use GRI Standards for their sustainability reporting.

Who It’s For

GRI is designed for a broad audience.

Unlike frameworks that focus narrowly on investors, GRI speaks to everyone — employees, communities, regulators, customers, civil society, and yes, investors too.

If your organization wants to tell a full, transparent story about how its operations affect people and the planet, GRI is built for that purpose.

How It Works

GRI uses a concept called impact materiality.

In plain English, this means you report on the topics where your organization has the most significant effect on the economy, the environment, and society — regardless of whether those topics directly affect your bottom line.

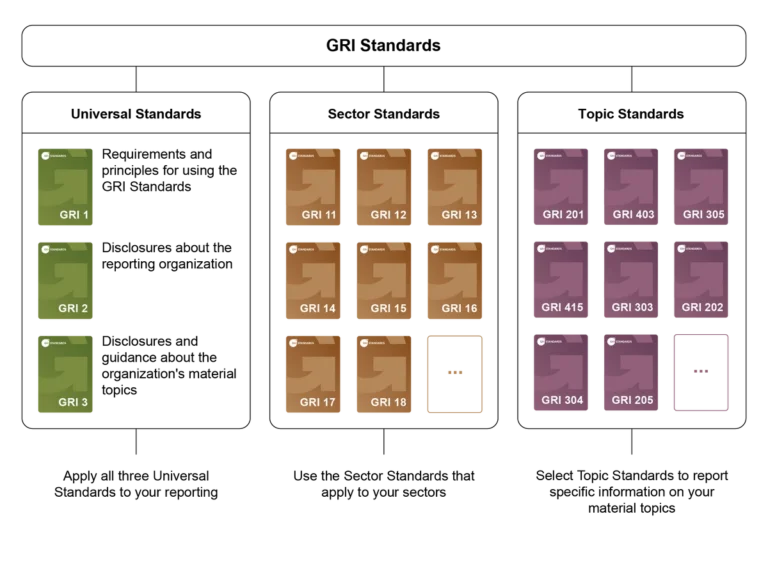

The standards are structured in three tiers:

- Universal Standards that apply to every organization (covering how you govern sustainability, how you determine what matters most, and general disclosures about your company).

- Sector Standards that address issues specific to your industry — oil and gas, mining, agriculture, and so on.

- Topic Standards that provide detailed guidance on specific subjects like emissions, water, labor practices, anti-corruption, and more.

Key Strengths

GRI’s biggest advantage is comprehensiveness. It’s the framework of choice when your goal is total transparency across all ESG dimensions — not just the ones that affect financial performance.

It’s also globally recognized, freely available, and well-suited for organizations that engage with a diverse set of stakeholders.

Companies preparing for their first GRI-aligned report often benefit from working with an experienced ESG consulting firm to conduct an initial materiality assessment and identify the most relevant disclosure topics before beginning the reporting process.

SASB: The Investor-Focused, Industry-Specific Standard

What It Is

The Sustainability Accounting Standards Board (SASB) takes a fundamentally different approach from GRI.

Rather than trying to capture a company’s full sustainability footprint, SASB zeroes in on the ESG issues that are most likely to affect financial performance within a specific industry.

It developed 77 industry-specific standards, each tailored to the unique sustainability risks and opportunities of a particular sector.

Who It’s For

SASB was designed primarily for investors and capital markets.

It’s the framework you choose when your main goal is communicating decision-useful ESG information to shareholders, analysts, and institutional investors.

How It Works

SASB uses financial materiality as its guiding principle.

Instead of asking “what are our biggest impacts on the world?” (the GRI approach), SASB asks “which sustainability issues could reasonably be expected to affect our financial condition, operating performance, or risk profile?”

This means the specific metrics you report depend entirely on your industry.

A software company and a mining company will have very different SASB disclosures, because the sustainability issues that affect their financial performance are different.

Key Strengths

SASB’s strength lies in its precision and comparability.

Because the standards are industry-specific, investors can compare companies within the same sector on a consistent set of metrics.

SASB also integrates well with mainstream financial filings — many U.S. companies include SASB disclosures directly in their annual reports or 10-K filings.

An important update: in August 2022, the SASB Standards were consolidated under the IFRS Foundation, and the International Sustainability Standards Board (ISSB) assumed responsibility for maintaining and evolving them.

The ISSB has committed to preserving SASB’s industry-based approach, so companies already using SASB are well-positioned for the transition to the ISSB framework.

If you’re managing SASB disclosures alongside other reporting obligations, investing in a purpose-built carbon accounting platform can help centralize your data collection and maintain audit-ready records across multiple frameworks simultaneously.

TCFD: The Climate-Risk Reporting Pioneer

What It Is

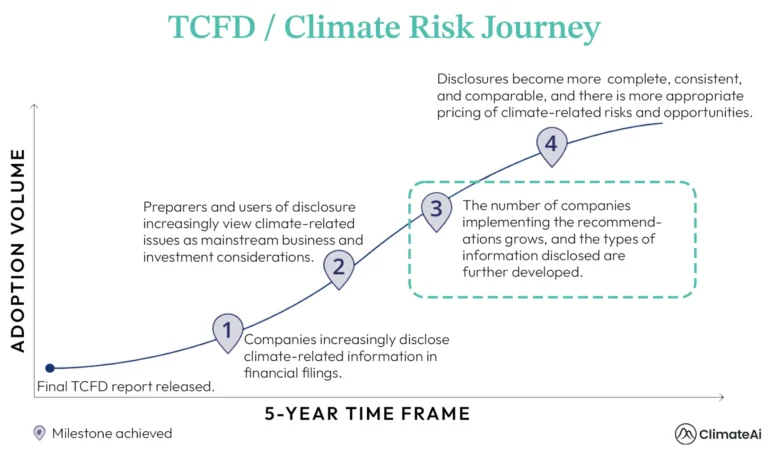

The Task Force on Climate-related Financial Disclosures (TCFD) was created in 2015 by the Financial Stability Board to help companies disclose how climate change affects their financial outlook.

Unlike GRI’s broad scope or SASB’s industry-specific approach, TCFD focuses specifically on climate-related risks and opportunities and their potential financial impact.

A Critical Update for 2026

Here’s something many organizations don’t realize yet: the TCFD officially disbanded in late 2023.

The Financial Stability Board declared that the ISSB Standards — specifically IFRS S1 and IFRS S2 — represent the “culmination of the work of the TCFD,” and monitoring responsibilities were transferred to the ISSB starting in 2024.

This doesn’t mean the TCFD framework is irrelevant.

Companies can still use the TCFD recommendations, and some jurisdictions (including the UK and Japan) continue to require TCFD-aligned disclosures.

However, the global trajectory is clearly moving toward the ISSB Standards, which fully incorporate the TCFD’s four-pillar structure: Governance, Strategy, Risk Management, and Metrics & Targets.

Who It’s For

TCFD was designed for financial stakeholders — investors, lenders, and insurance underwriters who need to understand how climate change could affect a company’s financial health.

It’s particularly important for organizations in high-exposure sectors like energy, agriculture, transportation, and financial services.

How It Works

The TCFD framework is organized around four pillars:

- Governance: How does your board and management oversee climate-related risks?

- Strategy: What are the actual and potential climate impacts on your business, strategy, and financial planning?

- Risk Management: How do you identify, assess, and manage climate-related risks?

- Metrics and Targets: What metrics and targets do you use to assess and manage relevant climate-related risks?

A distinguishing feature of the TCFD is its emphasis on scenario analysis — the practice of modeling how your business would perform under different climate futures (for example, a world that limits warming to 1.5°C versus one that reaches 4°C).

This forward-looking element gives investors insight into a company’s resilience and transition preparedness.

Key Strengths

Even though the TCFD has disbanded, its intellectual framework lives on through the ISSB Standards.

Over 4,800 organizations endorsed the TCFD recommendations before the transition, and its four-pillar structure has become the de facto standard for climate-related financial disclosure worldwide.

Organizations that have already been reporting under TCFD will find the transition to ISSB relatively smooth.

For companies navigating the shift from TCFD to ISSB, enrolling your team in a recognized ESG and climate risk training program is a practical way to build internal capacity and ensure your staff is prepared for the evolving disclosure requirements.

GRI vs. SASB vs. TCFD: A Side-by-Side Comparison

Let’s cut through the complexity and compare these three frameworks on the dimensions that matter most.

Primary Audience

- GRI: All stakeholders (investors, employees, communities, regulators, NGOs, customers).

- SASB: Investors and capital markets.

- TCFD: Financial stakeholders (investors, lenders, insurers).

What You Report On

- GRI: Broad ESG topics based on your organization’s impact on the economy, environment, and people (impact materiality).

- SASB: Industry-specific ESG issues that affect financial performance (financial materiality).

- TCFD: Climate-related risks and opportunities and their financial implications.

Scope

- GRI: Comprehensive — covers environmental, social, and governance dimensions.

- SASB: Focused — 77 industry-specific standards centered on financially material ESG issues.

- TCFD: Narrow — concentrated exclusively on climate-related financial disclosure.

Materiality Approach

- GRI: Impact materiality — how your business affects the world.

- SASB: Financial materiality — how ESG issues affect your business financially.

- TCFD: Climate-financial materiality — how climate change affects your financial position.

Current Status (2026)

- GRI: Active and widely used globally. Aligned with ISSB on GHG emissions methodologies since 2025.

- SASB: Now maintained by the ISSB under the IFRS Foundation. Standards remain active and are integrated into IFRS S1.

- TCFD: Disbanded in late 2023. Recommendations fully incorporated into ISSB Standards (IFRS S1 and IFRS S2). Still used in some jurisdictions.

Do You Need All Three Frameworks? (Spoiler: Probably Not All, But Maybe More Than One)

Here’s a reality that trips up a lot of organizations: these frameworks aren’t mutually exclusive, and they aren’t competitors.

They were designed to serve different purposes and different audiences. Many of the world’s most sophisticated reporters use a combination.

The key is understanding which combination makes sense for your situation. Ask yourself three questions:

- Who is my primary audience? If it’s investors, lean toward SASB (or ISSB). If it’s a broad range of stakeholders, start with GRI. If climate risk is the focal point, the TCFD/ISSB structure is your anchor.

- What does regulation require? If you’re operating in or selling into the EU, CSRD alignment is likely mandatory, and it builds on double materiality — which combines elements of both GRI and SASB thinking. In the UK and Japan, TCFD-aligned reporting may still be required.

- What do my customers and supply chain partners expect? Large corporations increasingly require their suppliers to report under specific standards. Know what your biggest clients are asking for.

The good news is that convergence is happening.

The ISSB has integrated SASB’s industry-specific metrics and the TCFD’s four-pillar structure.

GRI has aligned with the ISSB on greenhouse gas emissions reporting methodologies.

And the EU’s Omnibus Simplification Package has improved interoperability between CSRD and ISSB. The work you do for one framework increasingly carries over to another.

If you’re managing multi-framework reporting for the first time, a specialized ESG reporting platform can automate data collection across standards and reduce the duplication that makes compliance feel so burdensome.

How to Choose the Right Framework for Your Organization

If the comparison above still feels abstract, here’s a practical decision-making path you can follow.

Step 1: Start With Your Regulatory Obligations

Before choosing any voluntary framework, determine whether your organization is already subject to mandatory reporting.

If you fall under the EU’s CSRD, that’s your starting point.

If you’re a large company operating in California, the state’s climate disclosure laws may apply.

If you’re listed in a jurisdiction adopting the ISSB, those standards will become your baseline.

Step 2: Identify Your Primary Stakeholders

If investors are your main audience, SASB (now maintained by the ISSB) and the ISSB Standards should be your focus.

If you serve a broader stakeholder base — including local communities, employees, and civil society — GRI gives you the structure to address their concerns comprehensively.

Step 3: Conduct a Materiality Assessment

A materiality assessment helps you identify the ESG issues that matter most to your organization and your stakeholders.

For GRI, this means assessing your impacts on the economy, environment, and people.

For SASB/ISSB, it means identifying the sustainability topics that could affect your financial performance.

For the TCFD/ISSB climate pillar, it means evaluating the specific climate-related risks and opportunities your business faces.

Step 4: Build Gradually

You don’t need to adopt everything at once.

Many organizations start with a single framework, build their data infrastructure and internal capabilities, and then expand to additional standards as they mature.

Starting with GRI and layering in ISSB-aligned investor disclosures is a common and effective approach.

Step 5: Get the Right Tools and Support

Modern ESG reporting is data-intensive. Whether you’re tracking greenhouse gas emissions, workforce diversity metrics, or supply chain risk indicators, you need reliable systems for data collection, analysis, and audit-ready reporting.

Investing in dedicated ESG compliance software early in the process can save significant time and reduce the risk of errors as your reporting obligations expand.

The Bigger Picture: Where ESG Reporting Is Heading

The ESG reporting landscape is converging. The alphabet soup is gradually being simplified.

The ISSB is emerging as the global baseline for investor-focused sustainability disclosures. GRI remains the standard for broad stakeholder transparency. And the TCFD’s legacy lives on through the ISSB Standards that now carry its recommendations forward.

At the same time, new frontiers are opening. The Taskforce on Nature-related Financial Disclosures (TNFD) is gaining traction, with over 400 organizations already reporting voluntarily.

Biodiversity and nature-related risk disclosure are expected to become increasingly important as investors and regulators expand their focus beyond carbon.

For organizations just getting started, the message is clear: the time to build your reporting infrastructure is now.

The frameworks are maturing, the tools are improving, and the expectations from investors, regulators, and customers are only going up.

Final Thoughts: Frameworks Are Tools, Not Trophies

The biggest mistake organizations make with ESG reporting frameworks is treating them like badges to collect rather than tools to use.

A GRI report that sits on a shelf unread, a SASB disclosure that nobody in leadership actually understands, a TCFD-aligned climate assessment that doesn’t inform real business decisions — these are wasted opportunities.

The frameworks that matter are the ones that change how your organization thinks, plans, and operates.

The right framework is the one that connects sustainability performance to business strategy, helps you communicate credibly with the people who matter most, and builds the data infrastructure you’ll need as regulations and stakeholder expectations continue to evolve.

So don’t get paralyzed by the acronyms. Pick the framework that matches your audience, your regulatory context, and your ambition. Start building. And remember: the goal isn’t perfect reporting. The goal is meaningful reporting that drives real improvement.

Want to know which ESG reporting framework is the best fit for your organization? At Sustaenia, we help businesses navigate the evolving ESG landscape with clarity and confidence. Get in touch to start the conversation.